Stablecoins: Business Models and Future Shape of Marketplace

1. Why do we do it?

Living in the US, I regularly send money to Europe to fund day-to-day expenditure. Options to do so are plenty nowadays, however, speed and cost efficiency still varies widely. When sending money internationally, wire transfers are still the weapon of choice for many. Sending 1,000 USD from your Chase account to your EU SEPA account on July 28th 2024 would leave you with approximately EUR 890. Sending money via different fintechs, neobanks and remittance providers instead could leave you with up to EUR 917 and these players also provide for a very slick UX.[1] Using stablecoins such as USDC through providers such as Bitstamp, Kraken or Coinbase and a low-cost blockchain such as Stellar is the most cost-efficient way, leaving you with c. EUR 920.[2]

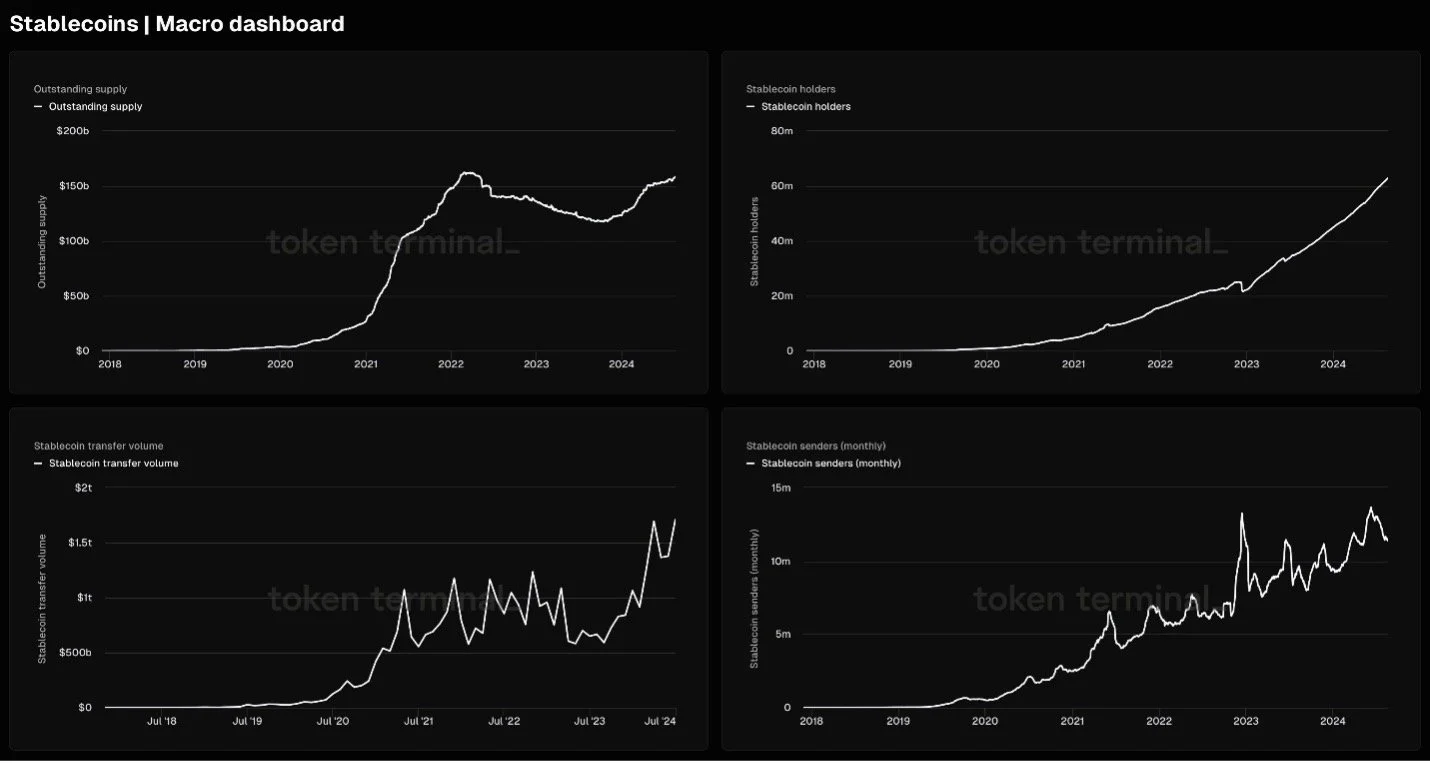

The more material the amounts the more material the difference. This is just one small example demonstrating the superior efficiency of stablecoins and blockchains to move value globally. Using stablecoins also enhances transparency of transfers as well as provides access to prevalent FX rates to individuals. Potential of stablecoins is undeniable. They’ve been dubbed crypto’s killer use case seeing sustained growth across key adoption metrics.

Figure 1 - Source: Token Terminal

However, blockchains and stablecoins still suffer from a sub-par user experience, oftentimes reserved for the crypto-savvy. The case in point involves opening accounts with multiple intermediaries, understanding of blockchain transfers and can be time-consuming.

And that’s why we do it. Market focus is shifting towards building blockchain-native user experiences on par with those seen in Web 2 while operating on more efficient rails. Usability improvements will drive the next phase of stablecoin adoption and new project are emerging that will trigger the market to meaningfully reshape.

This piece hopefully provides a small insight into current stablecoin demand drivers, speculates how marketplace might meaningfully reshape in the future and pieces of market infrastructure are important for its further growth.

2. Use cases and shape of the marketplace today.

Thus far, fiat-backed stablecoins have been an interesting experiment showing that there are too many fiat currencies in existence when the world seems to be quite happy transacting in a few. Stablecoin market today is dominated by USD-backed stablecoins, specifically by USDC and USDT. They are arguably the only ones that have managed to reach scale[3] with close to 95% market capitalization dominance in fiat-backed stablecoin market.[4] [5]

Besides their incumbent status, they can simply be seen as an onshore (USDC) and offshore (USDT) digital dollars. Their current relative strength gives insight into digital dollar demand profile, which seems to be primarily offshore.

Beyond that, it is very interesting to try understand what drives demand for various stablecoins. Currency (e.g. USD) exposure (i.e. short-term store of value) is likely the primary driver of stablecoin demand and a motive behind any other driver. Besides that, for simplicity, I distinguish the following 5 broad drivers of demand in no particular order - noting that surely more than 5 exist today:

Exchange Settlement Asset

DeFi

Payments and Commerce

Remittance

Treasury

Market size of each of the above categories is substantial.

Trying to visualise strength of above demand drivers for the leading stablecoin, USDT, radar chart could look something like this:

Being first to market, has enabled USDT to reach Exchange Settlement Asset (ESA) status across leading, non-fiat, offshore exchanges. USDT is so engrained in crypto’s offshore markets that there has been no project that would successfully challenge Tether’s ESA status despite its regulatory and commercial difficulties. Traders, exchanges and other distribution agents continue to use USDT despite the misalignment of economic incentives, arguably due to its staying power over the years and relative neutrality.

Another driver of USDT demand is DeFi where billions are locked in different L2 gateways and bridges.[6] Treasury, Remittance and Payments are harder to pin down; however, we know that USDT is used as asset-of-choice across many geographies, especially East Asia and LATAM both for money movement, corporate treasury purposes as well as payments.

These are also areas where I think Circle’s USDC is ahead due to its focus on developing cross-chain and payments infrastructure as well as establishing a robust regulatory footprint which makes it a good candidate for Corporate Treasury use cases. At the same time, it is unlikely that USDC reaches the ESA status offshore. This can provide an idea how the above visual could look for USDC.

In contrast, Paypal’s PYUSD and Societe Generale-Forge’s EURCV perceived drivers of demand are presented in the visual below.

Paypal’s existing merchant business is a great distribution channel for its stablecoin product. Connected to that, demand for PYUSD will likely through Remittance and Corporate Treasury use cases. At the same time, we’ve recently seen PYUSD expand aggressively to DeFi, especially on Solana blockchain, which is the leading PYUSD chain by market capitalisation.[7]

EURCV is an EUR-backed project backed by French giant Societe Generale. Due to its more traditional roots, we anticipate strong adoption as corporate treasury asset, settlement asset for tokenised financial instruments with possibly less usage in DeFi and Payments. An alternative focus could include dominating a specific Euro remittance corridor. As an Euro project, EURCV’s addressable market is substantially smaller compared to USD-backed counterparts.

Paypal and Societe Generale are two exceptionally strong and reputable issuers while more marquee names such as Deutsche Bank, Ripple, VanEck have also announced their market entry.

However, its worth noting that despite the substantial investment, PYUSD market capitalisation is currently around USD 0.8bn. USD 0.8bn is a commendable market capitalisation; however, still substantially smaller compared to USDC and USDT. This shows the difficulty of scaling stablecoins in a single-issuer model without a substantial initial investment. Given who the market leaders are today, projects can also develop alternative models for economic relationships between issuers, who provide the infrastructure and various distribution agents (e.g. exchanges, brokers, individuals, corporates), who facilitate demand.

Two additional very important factors also cannot be overlooked – geography and blockchain presence. As incumbents, USDT and USDC have strong global presence and can be bridged and used across various blockchains. However, there are notable discrepancies in market capitalisation across blockchains and likely across countries as well. For example, whilst Circle decided not to continue competing on Tron, which is dominated by USDT, USDC is currently the dominant stablecoin on Solana by a large margin.

We can slide and dice the visual above in many ways applying the lens of blockchain and geography focus. Some parameters are harder to pin that others and are arguably also a perception.

However, the underlying message should be clear:

Fiat-backed stablecoin market has been relatively rigid in terms of business models and scaling new stablecoins is difficult.

Projects entering the market should think carefully about their market positioning and focus use cases. Even if not immediately, revenue streams should go beyond the focus on growing market capitalisation.

Even if issuers are large and well-capitalised, they need to determine their focus. A niche, at least initially, can be a specific L1, a remittance corridor or a payments processor partnership. Being first in clinching an emerging ecosystem with a great UX can yield good results.

Single-issuer projects can consider rearranging stakeholder positioning and incentive models to reach scale faster.

A cohort of exceptional issuers is entering the fiat-backed stablecoin market in H2 2024, it is going to be very interesting to observe how they will face their scaling challenges and what new use cases will emerge.

3. How to reshape the marketplace?

I believe that shape of stablecoin market will change substantially in the next 3 years. This primarily be driven by regulatory clarity which will spur more institutions to take the leap. Looking at current use cases I believe many private monies will be operating at scale in the future. It’s not unreasonable for market capitalisation of fiat-backed stablecoins to reach $500bn in not-too-distant future and be a multi-trillion marketplace in 5 years’ time.[8] If 15% of the overall $500bn pie is reserved for non-USD stablecoins, that could also result in a $75bn market for those. A great opportunity.

In the USD-backed stablecoin market, challengers have a hill to climb if the marketplace is to meaningfully reshape. Amongst others, I see two unique, key challenges to overcome by issuers and other market participants.

Stablecoin issuers implementing models and incentive structures to reach network effects while appealing to broader range of market participants.

Issuers and infrastructure builders solving for a multi-chain world and the stablecoin fungibility problem.

3.1. Models and Incentive Structures

3.1.1. Models

Besides a single-issuer model (e.g. PYUSD), there are a few other, more or less tested approaches that we’ve seen issuers consider to reach scale faster. Model-to-model transitions are also possible as projects grow and evolve.

o Single-Issuer model:

Traditional model such as USDT or USDC.

Single-Issuer Distribution Model: Single-issuer models where majority of yield generated on invested assets is captured by distribution agents by default. This includes projects such as Agora, which launched AUSD in Q3-24.[9] This approach aligns incentives nicely but limits flexibility of distribution agents.

o Issuance-as-a-service:

Technology and Regulatory: A white-label model most successfully implemented by Paxos. It involves reliance on the issuer to provide technology and regulatory infrastructure whilst distribution agent provides branding and distribution. This is a fast path to market for many issuers. Alternatively, the distribution agent can obtain appropriate licensing (thereby becoming a legal issuer) and the issuer only provides the technology.

Technology only: In such a model, technology provider can take advantage of economies of scale if it provides services to more than one distribution agent; however, the model struggles to align incentives between different distribution agents.

o Consortium or multi-issuer approach:

Consortium-based approach was pioneered by Circle and Coinbase launching USDC back in 2018. They envisaged to slowly add more USDC issuers to Centre, who would govern the USDC protocol.[10] It is hard to envisage that the two giants would be revisiting their current approach, given overwhelming success USDC in its current shape.

Consortium of strong issuers can effectively super-charge distribution of the stablecoin early-on as stakeholders align incentives and leverage their joint distribution networks. This approach can also be viable if it evolves from Single-issuer models to boost distribution across products and geographies. It’s possible to envisage multiple different classes of stakeholders, incentive structures for those who add utility to the project and more.

In an example of a technology-only approach, company M^0 recently raised a $35M funding round to launch M cryptodollar, a federated middleware providing a turnkey approach for multi-issuance of fungible digital dollars which involves different groups of stakeholders and decentralized governance. An interesting solution providing a scalable, rules-based setup.[11] Decentralized, code-based or rules-based approaches are interesting due to their out-of-the-box scalability.

o Multi-issuer and multi-asset:

What will hopefully be an evolution of the consortium approach where different tokenised assets (e.g. various fiat currencies, wrapped cryptocurrencies, commodities) are issued by consortiums of issuers globally.

3.1.2. Incentive Structures

In terms of incentives split between different market participants, the problem of sustainable value capture split between infrastructure providers and distribution agents is not new to stablecoins. Different industries and businesses can serve as a valuable indication.

Uber will capture approximately 25% of the total ride cost as it providers the infrastructure for distribution agents (drivers).

Airbnb’s guest fee is c. 15% as it provides the infrastructure for its distribution agents (hosts).

In commercial banking, banks and brokers without direct access to European Central Bank overnight facility still capture up to 95% of the yield on their deposited Euro balances.

In some parts of the finance industry, such as clearing, stakeholders are aligned through distributed ownership structures.

If infrastructure providers in sharing economies captured more than 50% of the total transaction value or if a single commercial bank would own more than 50% of CHIPS clearing system, the market would likely quickly adjust and new infrastructure operating with a new set of incentives would emerge.

It is possible to expect that value capture of infrastructure providers in stablecoin space will likely trend lower over time with 10-20% capture being a longer-term equilibrium. Rest of the value will flow to project’s distribution agents and other stakeholders. As seen in other industries, over time, successful projects will identify and introduce new products and utility-based revenue streams to move away from dependence on yield generation.

3.2. Solving for a multi-chain world or the stablecoin fungibility problem.

I believe that within 5 years, to be successful, every bank or fintech will need to accept stablecoins just to stay competitive. I want to reiterate the belief that there will likely be many (i.e. more than 10) private monies operating at scale in the future. They will have different utility footprints, geographic coverages, and business focuses. If we believe that similar market dynamics will persist amongst layer-1 blockchains or equivalents, we end up with a matrix of non-fungible monies existing on non-interoperable blockchains, ultimately providing for a poor UX. This again is not a new problem but is one that hasn’t really been solved, at least for the fungibility part.

Some issuers, such as Circle are strongly focused on solving the interoperability issue by making it easy for developers to bring USDC into their chains and applications. Circle provides blockchain interoperability through CCCP.[12] This is an interesting approach that enables ecosystems to deploy Circle-compatible USDC without Circle’s initial cooperation also enabling backward compatibility of USDC contracts in such ecosystems when Circle is ready for a native deploy.

Multi-chain path is truly paramount for stablecoin issuers, yet developing and maintaining multi-chain infrastructure can be burdensome, especially for smaller projects. In addition, distribution agents need to connect to multiple issuers and various chains to be able to offer the service which requires a substantial development effort and keep-up and becomes a well-known question of business prioritisation.

Market is thus seeing the emergence of intermediaries solving for (stablecoin) interoperability and fungibility. Interoperability is relatively well advanced and being solved by various bridging solutions, while solving for fungibility and offering that as a service to market participants is relatively nascent. Both are in my view fundamental elements of stablecoin ‘plumbing’ infrastructure and are key for further adoption growth:

o Bridging involves sending (or bridging) a stablecoin on one chain and receiving it on a different chain. There are different types of bridges in existence. For example, native bridges developed by layer-2 chains such as Arbitrum and Optimism as well as 3rd party bridges such as Wormhole.

Bridge aggregators: Bridge aggregators take away the need for individual implementations by distribution agents. They chose the most optimal way for coins to travel across chains instead and provide for a single point of entry. For example, Socket integrated into Coinbase wallet.[13]

Beyond moving value from chain A to chain B, bridging in stablecoin context becomes even more interesting when it ‘packages’ more actions or transactions together. A receipt of payment from chain A to chain B automatically triggers a consequence or an action.

o Clearing / Abstraction involves sending in a stablecoin (or fiat) and receiving a different stablecoin on the same or different chain. This ultimately is a single-point-of-entry that moves the ‘matrix’ of integrations and relationships away from different market participants. It does, however, involve taking the other side of the trade by the provider, which introduces counterparty exposure, requires inventory and risk management and more.

Thus far, the closest approximation of this service has been provided by exchanges, which supported 1:1 swapping between various tokens. Service was enabled by Binance back in 2020[14] and is currently also available at Crypto.com[15] as well as with USDC within the Coinbase ecosystem. However, the incentive of exchanges is primarily not to offer this product as a service, rather to aggregate their balances in a preferred, often affiliated stablecoin.

When offered as-a-service, clearing can provide many interesting opportunities that are achievable by market participants with significantly less resources.

It can enable market participants to move across different stablecoins at scale, support one or many different stablecoins in their ecosystems with one or more stablecoins serving as points of entry. It can completely abstract away the need for distribution agents (e.g. merchants) to implement and support individual stablecoins or chains whilst making their businesses compatible with those products.[16] Use cases range from retail and payments acceptance to wholesale, bulk movement of various stablecoins between large financial institutions.

Companies such as bridge.xyz are currently innovating in this space, which is likely to grow extensively.[17]

Figure 2: A simplified graphic of 'Clearing / Abstraction' Layer

Businesses building various fungibility solutions could front-run demand by connecting to various issuers betting on future adoption, while issuers could gain a single point of entry into large distribution channels. This would increase the usability and interoperability of various stablecoins and thereby increase their odds of reaching scale.

Drawing from the CHIPS case, as clearing solutions would ultimately scale, ecosystem neutrality will be an important feature. A consortium-style approach or a joint venture between multiple industry stakeholders with economic stakes in the entity can be a superior, neutral way to scale this type of service. If a single solution would get too aligned with an individual ecosystem extending favorable treatment to certain ecosystems, this could trigger backlash by other participants.

Regardless of which exact path the market will take, stablecoin issuers are well-advised to consider compatibility and interoperability token’s fundamental features. Getting connected to the right infrastructure early can be an important advantage in a space where innovation is rapid.

Judging by market capitalisation, stablecoins are arguably blockchain’s greatest invention, after Bitcoin and Ethereum. For an untrained eye, the market might seem slow-moving but is full of opportunity in terms of use cases, emerging structures, and business models. This is confirmed by many new issuers entering or about to enter the market. Their innovation will eventually trickle into everyone’s day-to-day. Infrastructure to support market expansion is not fully in place today but it is being built rapidly in front of our eyes.

With additional regulatory clarity, the next 12-18 months are going to be exciting to watch.

References:

[1] https://wise.com/us/compare/ . Wise offers a very slick end-to-end user experience.

[2] Assuming funding Coinbase from Citi bank account using ACH with an Opt-in USDC settlement function, transferring USDC via Stellar blockchain to Kraken, exchanging for EUR at prevailing USDC / EUR exchange rate and withdrawing to a SEPA bank account. Sending EUR from Europe to land in USD bank accounts is even more cost efficient.

[3] $1bn in market capitalisation.

[4] https://defillama.com/stablecoins. Noting that FUSD market capitalisation is also above USD 1BN but its holdings are dominated by Binance at over 95% with a very particular use case being and are equally show of Binance’s strength as well as the difficulty of single players to reach scale in USD stablecoin markets.

[5] John Pennington recently provided an interesting classification: https://www.stablecoinstandard.com/thought-articles/itsnotjuststablecoins

[6] https://etherscan.io/token/0xdac17f958d2ee523a2206206994597c13d831ec7

[7] https://defillama.com/stablecoin/paypal-usd

[8] As of 7/30/2024 total stablecoin supply sits at around $165BN, c. $7BN short of all-time-high.

[9] https://www.agora.finance/

[10] https://www.circle.com/blog/coinbase-and-circle-co-found-the-centre-consortium

[11] https://www.m0.org/

[12] https://www.circle.com/en/cross-chain-transfer-protocol

[13] https://www.socket.tech/

[14] https://www.binance.com/en/support/announcement/binance-launches-1-1-conversion-function-for-selected-stablecoins-into-busd-360038499812

[15] https://help.crypto.com/en/articles/6660134-usd-bundle#h_cd53a4a2fb

[16] Recently, Coinbase recently enabled such service which enables sending USDT on Tron to Coinbase wallet to automatically receive USDC.

[17] https://www.bridge.xyz/